Turning 65? Already 65? Let's not wing it.

The 4 Parts of Medicare

Part A

Hospital Insurance

Inpatient stays, skilled nursing, hospice

Part B

Medical Insurance

Doctor visits, outpatient care, preventive services

Part C

Medicare Advantage

All-in-one private plan that replaces Original Medicare

Part D

Prescription Drug Coverage

Covers your medications, standalone or built into Advantage plans

Original Medicare

Original Medicare is the traditional, government-run health insurance program for people 65 and older. Some people under 65 also qualify if they have certain disabilities or specific health conditions. It's made up of two parts: Part A and Part B.

Together, they're a solid foundation but they're not the whole picture. Original Medicare only pays about 80% of your hospital and medical costs, leaving you on the hook for the other 20%. And there's no cap on it. One bad year health-wise and that 20% adds up fast.

That's why most people don't stop at Original Medicare. You've got two ways to handle that gap: Add a Medigap (Medicare Supplement) plan that picks up the remaining 20%, or Enroll in a Medicare Advantage plan, which bundles Part A, Part B, and usually Part D into one plan with its own out-of-pocket cap.

Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies that have a contract with Medicare to manage and administer your Medicare benefits. All your benefits coordinated under one Medicare Approved Health Plan. These plans have benefits from both Medicare Parts A and B and may also include extra benefits not on Original Medicare.

Plans typically have Low to No Monthly Plan Premiums and the Max-Out-Of-Pocket (MOOP) protects you with financial limits on how much you can spend on covered health services each year.

Some plans include Rx Coverage (MAPD), others do not (MA-Only). Plans can also offer benefits such as: Dental, Hearing, Grocery Card, Over-The-Counter (OTC), Vision, Flex Spending Card, Fitness Membership, and Transportation.

Medicare Supplement (Medigap)

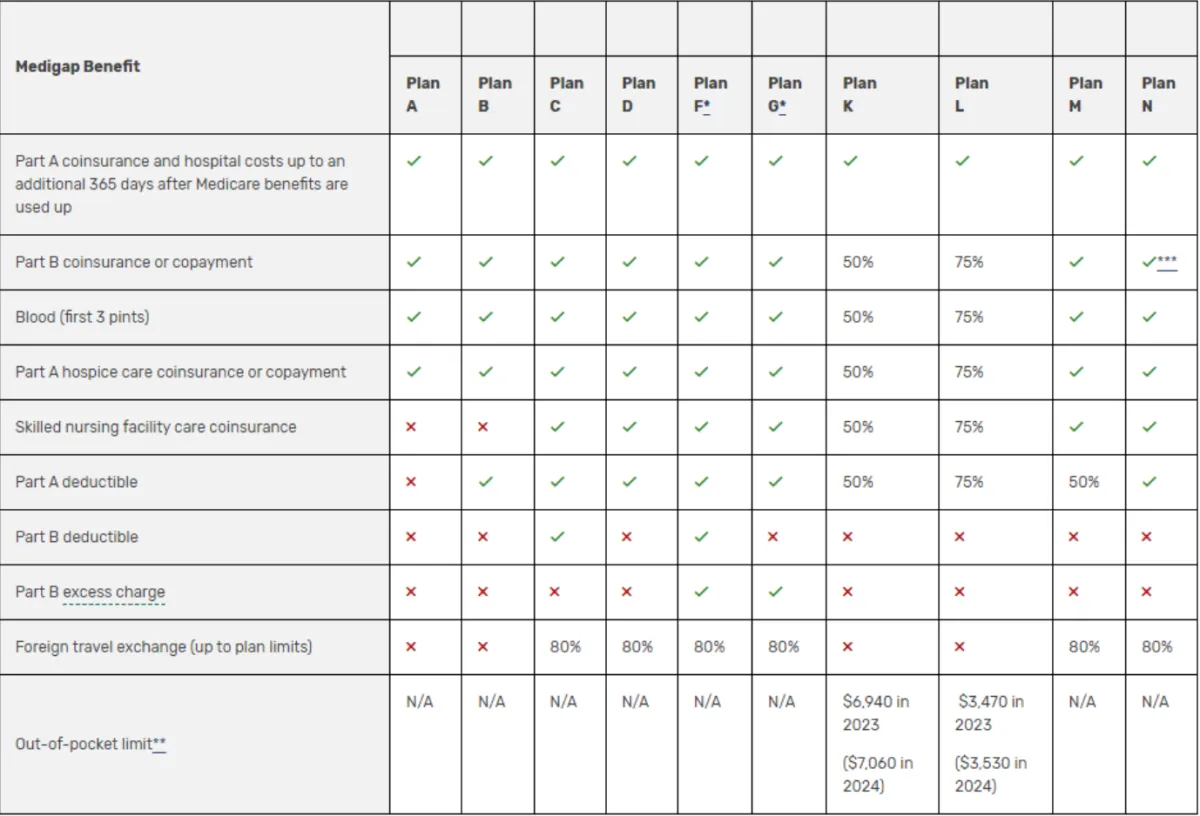

Medicare Supplement plans, also called Medigap, are private insurance policies designed to fill the gaps Original Medicare leaves behind. There are 10 standardized Medigap plans to choose from, each labeled with a letter.

Here's the deal: Original Medicare (Part A and Part B) covers about 80% of your hospital and medical costs but you're responsible for the other 20% with no cap on what you could spend in a year. Medigap plans step in to cover the remaining 20%, plus things like deductibles, copays, and coinsurance.

The result? Predictable costs. With most Medigap plans, you pay your monthly premium and very little when you go to the doctor or hospital.

Compare Medigap Plan Benefits

Medicare Enrollment Periods

Initial Enrollment Period (IEP)

The 7-month window around your 65th birthday 3 months before - the month you turn 65 - 3 months after. This is your first chance to enroll in Medicare. During your IEP you can sign up for Part A and Part B, a Medicare Advantage plan (Part C), and a Part D drug plan.

Initial Coverage Election Period (ICEP)

Your first window to choose a Medicare Advantage plan. Usually overlaps with your IEP. If you're going the Medicare Advantage route, this is when you can enroll.

Medigap Open Enrollment Period

A 6-month one-time window that starts the month you're 65 and enrolled in Part B. The most important window for anyone considering a Medicare Supplement (Medigap) plan. During these 6 months, you can buy any Medigap plan with no medical underwriting and no insurance company can deny you or charge you more for pre-existing conditions.

Annual Enrollment Period (AEP)

Every year: October 15 - December 7. Changes take effect January 1. This is the yearly window for anyone already on Medicare to make changes. During AEP you can switch from Original Medicare to Medicare Advantage (or vice versa), join, drop, or switch a Part D drug plan, or change from one Medicare Advantage plan to another.

Medicare Advantage Open Enrollment (MA-OEP

Every year: January 1 - March 31, one change allowed. If you're already on a Medicare Advantage plan, this is your one shot each year to switch to a different Medicare Advantage plan or drop your Advantage plan and go back to Original Medicare (with the option to add Part D). This window is only for people already on an Advantage plan and not for first-time enrollees.

General Enrollment Period (GEP)

Every year: January 1 - March 31. Coverage starts the month after you sign up. This is your safety net if you missed your IEP. You can enroll in Part A and/or Part B during this window, but coverage doesn't start right away and late enrollment penalties may apply (and can stick with you for life).

Special Enrollment Periods (SEPs)

Triggered by qualifying life events. Most give you 2-3 months to enroll. Certain events open a Special Enrollment Period outside the normal windows. You may qualify if: you lose employer or union coverage, you move out of your plan's service area, you qualify for Medicaid or Extra Help, or your plan's contract with Medicare ends.

We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE, or your local State Health Insurance Assistance Program (SHIP), to get information on all of your options.

Contact Info

Your future doesn’t fit into someone else’s mold… Let us help design yours…

Useful Links

Terms

© Copyright 2026 Generation 1. All Rights Reserved.